|

Taxes and Taxation

Правильная ссылка на статью:

Tikhonova A.V.

Architectonics of individual taxation system

// Налоги и налогообложение.

2023. № 5.

С. 27-53.

DOI: 10.7256/2454-065X.2023.5.43968 EDN: GRKPKW URL: https://nbpublish.com/library_read_article.php?id=43968

Architectonics of individual taxation system /

Архитектоника системы налогообложения физических лиц

Тихонова Анна Витальевна

ORCID: 0000-0001-8295-8113

кандидат экономических наук

доцент, ведущий научный сотрудник, Департамент налогов и налогового администрирования, Финансовый университет

127083, Россия, г. Москва, ул. Верхняя Масловка, 15, каб. 507

Tikhonova Anna Vital'evna

PhD in Economics

Associate Professor, Leading Researcher, Department of Taxes and Tax Administration, Financial University

127083, Russia, Moscow, Verkhnyaya Maslovka str., 15, room 507

|

samozvanka_89@bk.ru

|

|

|

Другие публикации этого автора

|

|

|

DOI: 10.7256/2454-065X.2023.5.43968

EDN: GRKPKW

Дата направления статьи в редакцию:

05-09-2023

Дата публикации:

06-11-2023

Аннотация:

Трансформация национальных экономик, вызванная глобализацией и цифровизацией бизнес-процессов приводит к изменению всей цепочки взаимоотношений на уровнях «государство-физическое лицо», «работник-работодатель», «налоговый орган – налогоплательщик». Цель исследования: разработать единый конструктив (архитектонику) системы налогообложения населения, учитывающую современные трансформационные процессы и основанную на применении принципов системной экономики. Методология исследования: качественный сравнительный анализ, имитационное моделирование и интерпретативные качественные исследования. Качественный сравнительный анализ использован для выделения элементов системы налогообложения физических лиц, имитационное моделирование – для визуализации ее основных параметров и ограничений, а интерпретативные исследования – для описания взаимодействия элементов системы (в контексте стагнации и эволюции). Основным результатом и научной новизной исследования является представленная архитектоника системы налогообложения физических лиц, развивающая теорию системной экономики Клейнера Г.Б. и включающая в себя 4 элемента (подсистемы), классифицированных по критерию определенности времени и пространства: 1) объекты – существуют в неопределенности времени и определенности пространства; 2) проекты – существуют в ограниченности времени и определенности пространства; 3) среды – существуют в неограниченности времени и неопределенности пространства; 4) процессы – существуют в ограниченности времени и неопределенности пространства. К элементам объектной подсистемы отнесены налогоплательщики физические лица и индивидуальные предприниматели, налоговые органы, налоговые агенты, иные участники налоговых правоотношений, территории. В проектную подсистему входят инструменты и механизмы налогового регулирования, носящие экспериментальный, временный характер. К средным элементам относятся системы налогообложения доходов и имущества физических лиц, налоговое законодательство, налоговые институты, налоговый климат, налоговая культура; к процессным элементам – информирование налогоплательщиков, налоговый контроль, налоговое администрирование. Автором охарактеризовано сочетание подсистем системы налогообложения физических лиц; а также визуализирована реализация функций налогов в контексте представленной системы.

Ключевые слова:

индивидуальный подоходный налог, имущественные налоги, системный подход, системная экономика, функции налогов, налоги на капитал, структура налогообложения, эволюция налогообложения, трансформация налогообложения, НДФЛ

Abstract: Transformation of national economies caused by globalization and digitalization of business processes leads to changes in the whole chain of relationships at the levels of "state-individual", "employee-employer", "tax authority-taxpayer". The following research goal is to develop a unified construct of the taxation system, taking into account modern transformation processes and system economy principles. The research applies a comprehensive approach, which includes three main analysis methods: qualitative comparative analysis, simulation modeling, and interpretative qualitative research. Qualitative comparative analysis was used to identify the elements of individual taxation. Simulation modeling was used to visualize taxation main parameters and limitations. Interpretative research was used to describe the interaction of the system elements. The scientific novelty of the research is the presented architectonics of individual taxation system, which develops the theory of system economy of Kleiner and includes 4 elements (subsystems), classified by the criterion of definiteness of time and space. First, objects – exist in the uncertainty of time and the certainty of space. Second, projects - exist in limited time and defined space. Third, environments – exist in the indefiniteness of time and the uncertainty of space. Fourth, processes - exist in limited time and uncertainty of space. The elements of the objective subsystem include taxpayers individuals and individual entrepreneurs, tax authorities, tax agents, other participants of tax legal relations, and the territory. The project subsystem includes tools and mechanisms of tax regulation, which are experimental and temporary in nature. Tax functions implementation was visualized in the context of the presented system.

Keywords: individual income tax, property taxes, systems approach, system economy, tax functions, taxes on capital, tax structure, evolution of taxation, tax transformation, PIT

Introduction

The development of modern society, increasing international integration, as well as the digitalization of business processes and robotization, are affecting the economies of all countries around the world. National tax systems are no exception. The same processes affect the existing labor relations, forms and types of employment, and therefore lead to the need to change individual taxation system. Only that tax system which meets the principles of system economy can function effectively. It allows taking into account all the diversity of economic relations related to income generation, ownership of property and other aspects of economic activity of the population.

The essence of the system approach is that when it is used, the object of research is first considered as part of a more general system, then it is considered as an independent system with all its essential elements and their functions. Then there is a combination of knowledge about the external environment with knowledge about the internal environment of the research object [1]. Systemic economics has one extremely important advantage in the context of this study: it is more comprehensively hierarchical from individuals as subjects of economic relations to mega-economic inter-state relations [2].

Traditionally, the system of taxation is understood as a set of taxes, fees and participants of tax legal relations. Nevertheless, the meaning of the system implies the presence of subordinate links between its elements [3]. In the context of scientific research on individual taxation, the main emphasis is placed on income taxation. At the same time, the importance of direct real taxes in the system of population taxation cannot be overlooked. The role of property taxation in the system of taxes levied on the population is extremely important, despite the much lower fiscal burden [4]. Real estate tax policy affects how capital gains should be taxed, due to the substitution of residential and nonresidential capital [5, 6]. Thus, the systemic synergistic effect of various taxation instruments is manifested.

A number of economists in their studies have repeatedly noted the haphazard nature of individual taxation [7]. For example, in the Russian Federation (RF) there is an inconsistency in the nominally existing elements of the mechanism of tax regulation of the household sector. A similar problem is observed in the taxation of individuals in European countries, in particular, in Hungary the package of tax policy measures has increased income inequality of the population [8]. The system approach allows one to eliminate the above contradictions of taxation, as it has a number of very important advantages.

First, the construction of any system involves achieving the principle of emergence, which is manifested in the achievement of synergistic, multiplicative effect due to the interaction of all its elements. Taking into account the importance of implementing not only fiscal, but also social, regulatory functions of individual taxation [9], this property seems to be fundamental. The problem of low performance of tax regulators against the background of budgetary support of the population is now characteristic of many countries in the world, including the Russian Federation [10], Finland, France, Germany, Belgium, Spain, Great Britain, Czech Republic, Romania [11]. In Switzerland, which demonstrates an astounding degree of stability in the redistribution and concentration of after-tax income, it is fiscal federalism that actually contributes to maintaining exceptional long-term stability [12].

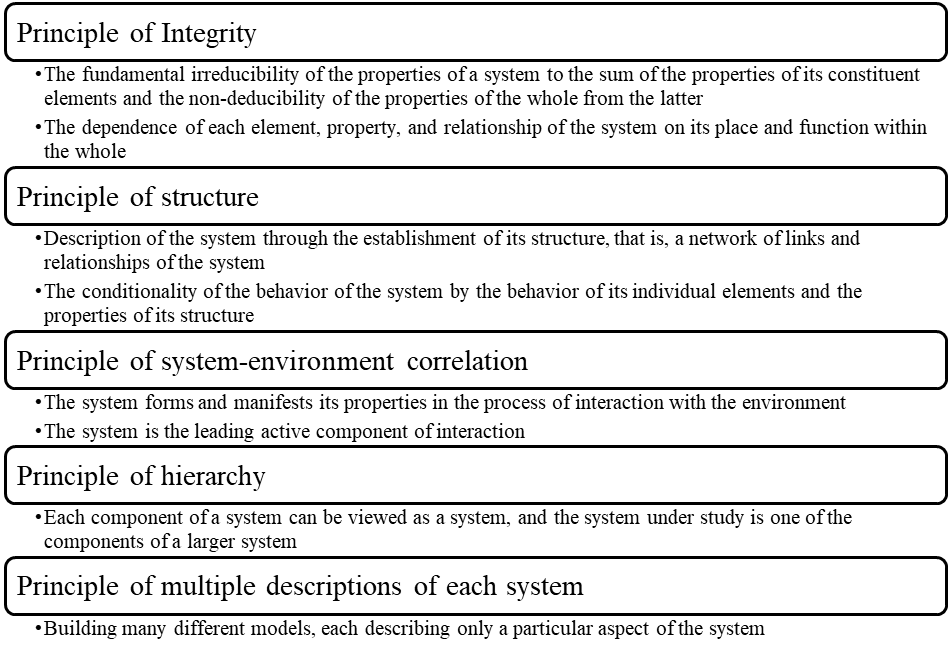

Second, the systemic construction of individual taxation allows for a holistic inseparable approach to all stages of tax administration (planning, taxation, control). As Nicolis and Prigogine point out, the behavior and structure of the system are one and the same and arise from self-organization rather than top-down control [13]. In this context, it is important to implement the taxation system principles (Figure 1).

Figure 1. Principles of system formation

The principles of classical system analysis presented above can manifest in individual taxation system. The principle of integrity implies that the maximum regulatory effect of taxes levied on citizens is achieved with the simultaneous action of the whole system. In this context, the development of income taxation without taking into account property or indirect taxation can significantly reduce its effectiveness.

The principle of correlation between the system and the environment is extremely important, which is manifested in the fact that the development of individual taxation system should take into account the "ecosystem". The latter includes the national economy, integration into the world community, structure and sources of income of the population, digitalization of social relations, behavioral motives, living standards and incomes of citizens, etc. For example, income is one of the factors in the transformation of approaches to individual taxation (Table 1).

Table 1. Analysis of Structural Shifts in the Russian Federation's Monetary Income, 2000-2020

|

|

Specific weight of income type in 2000 (d0), %

|

Specific weight of income type in 2020 (d1), %

|

Specific weight difference (d1-d0), percentage points (p.p.)

|

|

Income from entrepreneurial activity

|

15.4

|

5.2

|

-10.2

|

|

Property income

|

6.8

|

4.4

|

-2.4

|

|

Other income

|

27.5

|

11.1

|

-16.4

|

|

Compensation of labor

|

36.5

|

58.5

|

22

|

|

Social transfers

|

13.8

|

20.8

|

7

|

|

Total

|

100

|

100

|

X

|

Source: compiled by the author based on Rosstat.

The analysis of the structure of monetary incomes of the population (by sources of income formation) in the period from 2000 (the period before the introduction of Chapter 23 of the RF's Tax Code, which establishes the rules of taxation of personal income) to 2020 showed significant shifts. Namely, the share of labor remuneration increased by 22 p.p., while the share of income from entrepreneurial activity decreased by 10.2 p.p., and other income - by 16.4 p.p. Such serious changes predetermine the necessity to transform the system of income taxation. This transformation is typical not only for the Russian Federation, but also for a number of other countries, as evidenced by scientific research. According to the latest report of the International Labor Organization (hereinafter ILO), the share of global labor income in 2017 was 51.4%; 48.6% of income went to capital owners.

It is important to note that in recent years, the share of income from capital has increased and the share of income from property has decreased, which may be a factor in changing the system of property taxation as well [14].

In the context of the influence of behavioral motives, the study analyzes the possibility of introducing various inheritance and gift taxes, the need for which depends on the tax susceptibility of individuals. Studying the German experience, Glogowsky (2021), a professor at Johannes Kepler University in Linz, showed how the German inheritance and gift tax affects the behavior of the wealthy. Individuals tailor their taxable remittances and plan bequests to reduce their tax liability [15]. However, neither the general gift response nor the inheritance response has much effect on tax revenue collection: the associated short-term net tax elasticities of taxable wealth transfers lie below 0.1.

The principle of hierarchy suggests that the system of taxation of individuals should be logically built from subsystems of taxation of income, property, administration, and itself integrated into a unified tax system of the country. In this case, each of the subsystems is formed taking into account the classical principles noted in Figure 1. In this context, it is extremely important to note that individual taxation system should be dualistic, representing an element of a unified system of social support (it is considered in more detail below). On the one hand, the manifestation of the system approach in social policy is also aimed at implementing the principle of emergence and achieving a multiplicative effect. On the other hand, as noted by Ksiropulos (2017), tax measures have two significant institutional limitations: the first is the impossibility of identifying the tax component in the total effect of state financial support to citizens; the second is manifested in the impossibility of quantifying the effect achieved [16].

Third, the realization of the above-mentioned advantages contributes to a better achievement of the principle of equity. First of all, this is achieved through logically built internal relationships between the elements of the system of tax and budget support. It was noted above that the social effect of tax support is very difficult to assess, but in this context, when building a unified system of fiscal incentives, it is not always necessary to separate such an effect. It can be assessed through a system of social indicators, responding to the applied instruments of public policy. Such indicators may include the effective tax rate, real disposable income, the share of the population with incomes below the subsistence minimum or slightly above it, and the unemployment rate. It is possible to determine the optimal combination of fiscal instruments of regulating individuals, for example, in the framework of implementing the experimental approach (on the example of several regions). The latter is currently used in taxation of the self-employed in RF. Thus, consistency is directly related to the characteristics of tax fairness.

Fourthly, rationally built economic systems have the property of harmony, which achieves integral spatial and temporal balance and integrity of the system under the condition of sustainable evolutionary development. A harmonious economy has a powerful internal potential for overcoming contradictions within the framework of evolutionary development [17].

The relevance of developing individual taxation in the context of the system is also confirmed by the fact that the systems exhibit adaptability: the actions of individual agents lead to continuous changes in the system, which allow it to adapt to changing conditions [18]. This advantage is decisive in accelerating pace of international economic transformation.

Thus, modern changes in the incomes of individuals, mechanisms, and ways of their receipt are a global trend. The necessity of developing individual taxation as a unified economic system, taking into account the changes, is noted. This leads to the expediency of forming theoretical and methodological foundations of the system approach in population taxation, universal for any economy of any country in the world.

Analysis of scientific works in this area showed the lack of specialized literature defining individual taxation system itself, its territorial, spatial, and temporal limitations, constituent elements, as well as the principles of construction. This circumstance determined the objectives of the present study:

- to develop the architectonics of individual taxation system, universal for any country and integrated into higher level economic systems (tax system of the state, system of social support of the population, etc.);

- to define mechanisms of interaction of the system and driving forces of its evolution as a self-organizing organism.

Taken together, these elements represent the scientific novelty of the article and significantly distinguish it from previous works in the analyzed area.

Materials and methods

Having studied the literature on economic systems, it can be said that it would be useful for scholars to apply mixed (quantitative and qualitative) methods, as suggested by А. Najmaei [19]. In particular, three methods below are used: qualitative comparative analysis, simulation modeling, and interpretive qualitative research.

Qualitative comparative analysis is a configurational approach used to study phenomena that are best understood as clusters of interrelated structures and practices rather than as modular or loosely connected entities whose components can be understood in isolation [20]. Thus, different configurations of individual tax system components are likely to result in "causal asymmetry" and "equal results" [21]. This suggests that traditional methods of analysis, based on the assumption of linear relationships, are poorly suited to the study of economic systems because of the multicollinearity, non-normality of the data and the inability to consider the opposite cases [22].

Simulation modeling was used in the work to visualize the parameters and principles of individual taxation system. Scientists from various disciplines have used formal simulation models to study the behavior of complex systems [23].

Although quantitative methods are the dominant approach to the study of systems in other disciplines, qualitative methods (and data) are also well suited to the study of economic systems, including complex tax systems, for several reasons. First, economic systems (as noted above) are characterized by nonlinear dynamics, feedback loops, and complex multi-level interactions. The flexibility of qualitative methods makes them particularly suitable for studying such phenomena [24]. Second, communication between participants in tax legal relations is a process that both creates and constitutes the interaction of the economic system. It is through narratives, discourse, and other linguistic constructs that knowledge, fiscal values, and tax culture are transmitted between participants. Finally, the vividness and concreteness of qualitative data make them well-suited for comparison with some of the more abstract quantitative methods, since qualitative data can illustrate abstract ideas or make conceptual frameworks more concrete and understandable [24].

The methodological design of the study includes several stages:

Stage 1. Determining the elements of individual taxation system by extrapolation method, based on the transposition of the basic elements of Kleiner's economic systems to the individual taxation system. In the framework of this stage, two procedures were implemented:

1) formation of the spatial and temporal grid of the system and distribution of subsystems on it;

2) a detailed description of the elements of subsystems of individual taxation system.

The result of this stage is the constructed architectonics of the taxation system, presented in the first part of the study results.

Stage 2. Formation of mechanisms and effects of interaction of system elements by methods of casual and dialectical analysis. In the framework of this stage, two procedures were also implemented:

1) identification of cause-and-effect relationships between the individual elements of the system by the causal analysis method. This allowed highlighting the peculiarities of interaction between subsystems of individual taxation system through the prism of the principles of its functioning;

2) formation of an integrative approach to describing the combination of all subsystems of individual taxation system, as well as highlighting the possible negative effects of distortions in their interaction by method of dialectical analysis.

Stage 3. Disclosure of the functions (fiscal, social, control, regulatory) of taxes within the framework of the new individual taxation system using the tools of simulation mathematical modeling. This stage includes the following procedures:

1) substantive formulation of the problem (specification and allocation of tax functions for modeling purposes);

2) conceptual and mathematical formulation of the problem (formation of a system of 4 linear equations).

The results of scientific research on the system economy and taxation of individuals were used as a data set. Accumulated practical experience in applying instruments of tax regulation (on the example of the Russian Federation) was also used. Quantitative data were not analyzed at this stage of the study.

However, the presented methodological approach also has some research limitations. In particular, as noted earlier, economic systems arise as a result of nonlinear processes and interactions. However, when trying to build simulation models, as a rule, there is a complete linearization of relations in the system, thereby reducing or eliminating its complexity. Unfortunately, this also leads to a lack of ability to get an accurate picture of the subtleties of tax systems. In addition, the significant use of theoretical research methods in the work leads to some other possible limitations. First, the identified negative effects arising from the skewed interaction of system elements are based solely on the expert opinion of the author of this study, as well as a review of Russian individual taxation practices. Thus, these methods form a certain isolation of the researcher's thinking from the real conditions of the external environment. Secondly, for practical testing of the mathematical model and the construction of simplex tables it is necessary to have an array of closed data, access to which is available at the level of national tax authorities, which is a significant methodological limitation. It can, however, be avoided by conducting a chain of sequential laboratory experiments involving volunteer individuals and then extrapolating the results of the sample to the general population.

Results

Architectonics of Individual Taxation System

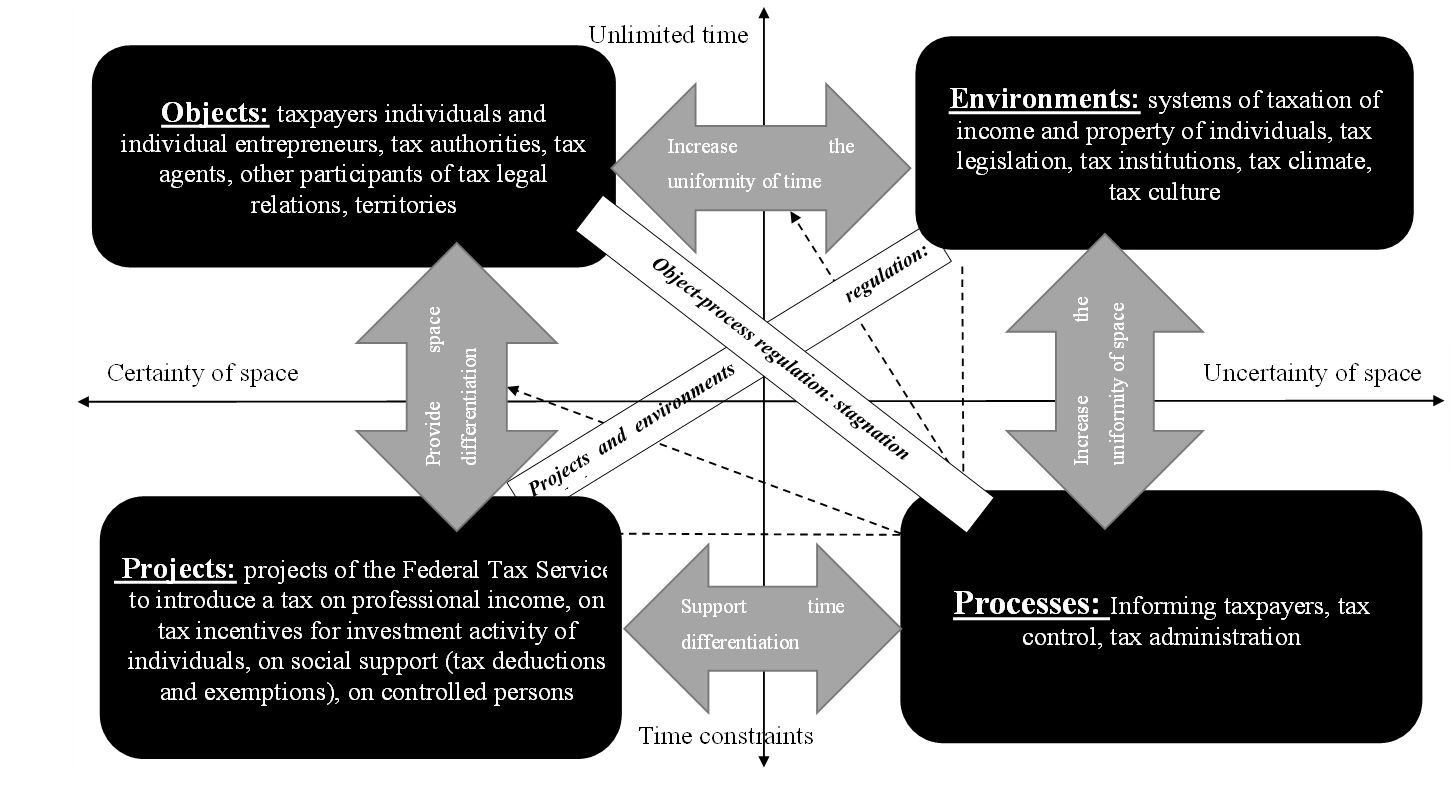

To form an individual taxation system, Kleiner's theory of economic systems was used. The author determined that any system operates in the space-time grid, based on which classified all systems into 4 groups:

1) objects are systems operating under the uncertainty of time, but in the certainty of space;

2) projects are systems that operate under conditions of limited time and certainty of space;

3) environments are systems that operate under conditions of unlimited time and uncertainty of space;

4) processes are systems operating under conditions of limited time and space uncertainty.

It seems that individual taxation system in the author's interpretation in the context of Kleiner's classification is an environment. At the same time, like every complex system, it consists of many other systems and is effective only in conditions of harmonized interaction of the systems of all four types.

Object subsystem includes taxpayers, tax authorities, tax agents and other participants of tax legal relations. In the context of implementing territorial tax policy (at the level of a region, municipality, zones with preferential tax regimes), a country's regions, as well as territories and international integration associations can act as elements of the object subsystem. For instance, special rules of personal income taxation are currently envisaged by the legislation of the member countries of the Eurasian Economic Union (EAEU), which is also a manifestation of the object subsystem of individual taxation system. It is important to note that the spatial boundaries (certainty of space - on the X-axis, Figure 2) of the object subsystem are defined by the following characteristics:

1) criteria of residency of individuals;

2) the location of the property;

3) the place of economic interest of natural persons;

4) criteria of recognition of the actual recipient of income;

5) criteria of interdependence and controllability;

6) the digital "presence" of an individual.

Figure 2. Individual taxation system (the author's interpretation)

It is worth noting that one of the reference points of the transformation of modern individual taxation system is precisely the characteristics of the spatial boundaries of the object subsystem. If the first three have been traditionally used in the world and Russian practice, then the 4th and 5th criteria represent the manifestation of modern world trends in taxation. The regulatory aspect of controllability has been actively used in the taxation of citizens recently, for example, since January 1, 2020 in the Russian Federation a fixed tax on profits of controlled foreign companies (CFC) has been applied.

The author's addition is the digital "presence" of the individual, which is currently not fully reflected in the tax practice of any country in the world. OECD and other international organizations are actively developing the concept of digital permanent representation for legal entities, but individuals are rarely mentioned. However, given today's level of digitalization, it is unlikely that the moment is far off when a citizen physically staying in one place will be fully engaged in the interests of another state with virtual assets and income in their digital field.

It is also worthwhile to make a few remarks regarding the already established criteria. The recognition of an individual's residency, which affects the size of the tax base and the tax rate on the territory of the Russian Federation, raises questions. The Russian concept of residency is based only on territorial criteria, namely the actual presence of a citizen on the territory of the country. However, international integration and globalization are blurring the economic borders of countries, and the criteria of physical location are no longer sufficient. A number of countries approach the definition of residency based on two criteria (location and place of economic interest). It is advisable to extend this approach to Russian practice as well.

The project subsystem includes the implementation of various projects of national ministries and tax authorities, in particular, the Ministry of Finance and the Federal Tax Service of the Russian Federation on:

- introduction of a tax on professional income;

- tax incentives for investment activity of individuals;

- social support (tax deductions and exemptions);

- controlled persons.

As Kleiner notes, project systems usually have both a certain spatial localization and a known start and end date of operation [17]. With regard to individual taxation system, the project subsystem has its own spatial boundaries (the certainty of space - on the X-axis, Figure 2), which are defined by the following characteristics:

1) regional (zonal) division;

2) the socio-cultural status of individuals;

3) material status.

It is important to note that the author's interpretation of the project systems involves only temporary tools of taxation and tax control, permanent tools form the subsystems of the environment. In particular, the Russian practice has in its asset the project on income taxation of the self-employed, the spatial certainty of which is determined by the regional division (initially for 4 regions of the Russian Federation) and the material situation (the limit on the total amount of income - 2.4 million rubles).

Characteristics of individuals' socio-cultural status are their social status (orphan, disabled, etc.) or belonging to a particular cultural group (peoples of the Far North, etc.).

Financial situation is a very broad characteristic, since it can be expressed both in the amount of active and passive income, and in the value of the property owned (for the purposes of property taxation), and a number of other aspects.

It should be noted that it is advisable to pay special attention to the development of the project subsystem in the context of a dynamically developing world, digitalization of the economy, globalization and integration. The factors of modern transformation of individual taxation system lead to the necessity of global restructuring of a number of environment subsystem elements. This restructuring is complicated by the sometimes weak technical capabilities of tax control at the international level (with the digitalization of the global economy and the blurring of tax bases), and therefore requires a long development of solutions. It is at this point that temporary tax projects are replacing outdated tax tools. Examples of such practices are already being reflected in the taxation of digital giants, with recent studies repeatedly suggesting the possibility of a temporary digital tax until countries develop a common unified approach in the tax administration of digital giants [25].

The environment subsystem includes the following elements: systems of taxation of income and property of individuals, tax legislation, tax institutions, tax climate, tax culture. The presented subsystem has no clear spatial definition and can function indefinitely. In taxation, the environment subsystem creates the institutional elements necessary for the successful functioning of individuals. Based on these conditions, spatial characteristics of environment subsystem are not formulated in the study. It is important to note that environment subsystem includes the tax tools, which have a permanent non-experimental nature. In addition, according to the author's understanding of the construct of individual taxation system, it seems inappropriate to include indirect taxes, which certainly affect the aggregate result of applying taxation mechanisms, in the composition of environment objects. Since individuals are only carriers of indirect taxes, the latter rather form the external ecosystem of taxation.

The process subsystem is about informing taxpayers, tax control, and tax administration. The process subsystem, like the environment subsystem, has no defined spatial boundaries (can be applied to any taxpayer in any territory of the country, and in some cases - at the international level). Consequently, the characteristics of spatial constraints are not applicable to it.

At the same time, unlike the environment subsystem, the functioning of the process subsystem traditionally requires "refill" from certain objects, otherwise they cease to work effectively. This property is most clearly manifested in the subsystem of tax control. Showing an opportunistic attitude, taxpayers create various schemes of evasion from taxation, while the development of tax legislation and forms of tax control generate new schemes of evasion. Thus, the effective functioning of the process subsystem of tax control is possible only in constant development on condition of the push behavior of the object subsystem of taxpayers.

Interaction of subsystems of individual taxation system

The system can only function effectively if all of its subsystems are in a certain proportion and work simultaneously in pairs:

1) environment subsystem - object subsystem;

2) object subsystem - project subsystem;

3) project subsystem - process subsystem;

4) process subsystem - environment subsystem.

In the context of individual taxation system, environment subsystems are aimed at increasing homogeneity in space and time. That is, they form the permanence and stability of taxation for the future (the first highlighted principle of individual taxation system). This creates fixed conditions for taxpayers' activity and is one of the classic conditions for the functioning of any tax system. It is the environment subsystem that creates the necessary prerequisites for comfortable activities of individuals, forming the tax climate and tax culture of citizens.

The object subsystem provides diversification of space, but at the same time it is homogeneous in time. It is important to note that such manifestation of object subsystem's properties is possible only on condition of its simultaneous interaction with the environment subsystem and the project subsystem (thus manifests the second principle - the principle of coordination). In the first case, an identical tax environment for all subsystem objects is formed, in the second - on the contrary, the conditions of taxation or tax administration are separated.

Finally, of the greatest interest from the standpoint of transformation of individual taxation system and evolutionary fiscal transformations are project and process subsystems. The first ones are the most dynamic subsystems, they ensure system diversification in time and space. Thus, it is the projects in taxation that are evolutionary drivers and contribute to the development of the entire individual taxation system (their work manifests the principle of system dynamism).

Process subsystems increase the homogeneity of space, but at the same time support the differentiation of time. In taxation the role of process subsystems is difficult to overestimate, as they provide interconnection between other system elements, implementing the provisions of the environment subsystem and the project subsystem. It is the process subsystems that are responsible for the implementation of social justice and the regulatory aspects of taxation, as they ensure the "conductivity" of the system and redistribution of public goods (thereby implementing the principle of synergy).

Individual taxation system is dual. This duality manifests itself in several aspects, which the study refers to as Principle 2D:

1) it should be logically integrated into the overall tax system of a country and be part of a country’s social policy system;

2) the work of the system involves the simultaneous performance of the fiscal function, realized in the replenishment of the budget, and the social function, presented in the form of budget expenditures (Figure 3).

Figure 3. Duality of individual taxation system

Source: compiled by the author.

The tetrad scheme of the three systems presented in Figure 3 is unique in scientific theory and practice. It demonstrates that a well-built individual taxation system is a link, a "conductor" between the tax system of a country and its social policy. In this interaction, the two most important functions of personal taxation manifest themselves: fiscal and social. On the other hand, it is important to note that social policy and the tax system form the ecosystem of individual taxation system, they give impulses and fill the space for its development.

Taxation system and functions of taxes

Another, no less important point, is the implementation of tax functions within individual taxation system. 4 functions were identified: fiscal, control, regulating and social, which should be reflected in the architectonics of the system. In order to visualize these functions, linear programming tools were used. In particular, for a general representation of tax system's architectonics, it is formalized into a system of 4 linear equations characterizing 4 tax functions, respectively.

The author's model has a theoretical character, since it is designed to study general regularities and properties of economic systems and has a macroeconomic aspect. When building mathematical models in economics, it is necessary to take into account that most characteristics of such models cannot be defined precisely. Their values are influenced by many unmeasured factors (including human, political, and other factors). As a result, the characteristics of economic models turn out to be random values grouped around some average values or averaged dependencies. For this reason the mathematical model of individual taxation system will have a stochastic form.

The first function is fiscal. The name of this function defines the purpose of the first equation of the system - to maximize tax revenues to the consolidated budget of the country (F1). Below is a mathematical representation of the fiscal function (formulas 1, 2).

(1) (1)

or

, (2) , (2)

с – effective rate of the j-th tax levied on individuals;

j – ordinal number of the tax levied on individuals;

xj – national tax base for the j-th tax levied on individuals.

To assess fiscal function implementation, the best indicator is the volume of tax revenues from taxpayers-individuals, which is proposed to estimate in the framework of macroeconomics as the product of the effective tax rate and the national tax base for each tax. The following constraints characterizing the dynamics of the most important socio-economic indicators should also be applied to the equation of fiscal function maximization (formula 3).

, (3) , (3)

p – official unemployment rate;

s – average per capita real disposable income of the population;

I – official inflation rate;

Tax – volume of tax revenues from individuals;

n – current year;

n-1 – previous year.

Thus, the main task of individual taxation system is not just nominal maximization of the volume of tax revenues, it must take into account the solvency of taxpayers, without reducing their real disposable income and without increasing unreported employment and unemployment.

The second function is a control function. The purpose of the second equation of the system is to minimize the amount of illegal employment (F2). The reduction of the shadow economy is the most important manifestation of an effective tax system; in the context of individuals, this manifests itself mainly in the reduction of the number of citizens both working entirely illegally and not receiving all their wages officially. Since the direct number of workers working illegally is impossible to estimate with high accuracy, the study uses the number of citizens who receive a minimum wage. A large part of them (especially in urban areas) form the shadow economy. Below is a mathematical representation of the control function (formulas 4, 5).

(4) (4)

or

, (5) , (5)

a – the size of the national minimum wage;

b – the number of employees who receive minimum wage;

i – region number;

k – the average ratio of the estimated amount of hidden wages to the national payroll.

To assess control function implementation, the best indicator is the minimum estimated amount of hidden wages. It is estimated in the framework of macroeconomics as the product of minimum wage, the adjustment coefficient k, and the number of employees who receive minimum wage. The following constraint characterizing the dynamics of the unemployment rate (formula 6) should also be applied to the equation maximizing the control function.

(6) (6)

Formalization of such a restriction will make it possible to take into account the situation in which citizens who previously showed their income at least in the amount of the minimum wage may go into unreported employment. In addition, another restriction for the equations characterizing fiscal, control, regulatory, and social functions of taxes is the non-reduction of tax revenues.

The third function is regulatory. The purpose of constructing the third equation of the system is to reduce the income gap of the first 5 deciles by income level (F3). In more detail, this model and its validation (the only one possible to calculate due to the lack of necessary open data) are presented earlier in the author's studies (formulas 7, 8) (Tikhonova, 2019).

(7) (7)

or

, (8) , (8)

d – the average per capita cash income of a decile.

The fourth function is the social function. The most difficult is to visualize the results of the social function of taxes in the context of individual taxation system, because aspects of social function manifestation are multifaceted, many of them are new and have not yet been studied well enough. As an example, suffice it to mention such a manifestation as its impact on the medical care of the population. Italian economists have proven that tax exemptions have a significant impact on tax revenues and introduce significant inequalities in access to health care for individuals in the Italian National Health System [26]. In this regard, it seems relevant to formalize the fourth function through a set of indicators reflecting the social development of society (to some extent, these indicators duplicate the indicators of social effectiveness of tax benefits). They are called "social indicators", which are indicators describing the provision of housing and household goods, health care, education, culture, as well as other social services (charity, support for people with disabilities, etc.). The purpose of constructing the fourth equation of the system is to maximize the value of the integral indicator of the social effect of tax benefits (F4). It is important to note that the actual distribution of personal income is a manifestation of the regulatory function, and therefore it is embedded in the equation F3. Below is a mathematical representation of the social function (formulas 9, 10).

(9) (9)

or

(10) (10)

m – specific weight (significance) of the social indicator, the normative value determined by the researcher;

f – growth rate of the social indicator;

e – ordinal number of social indicator.

The growth rates of social indicators are used as the basis for the fourth linear function, as they allow one to avoid the scale effect and give the system of functions the property of dynamism. The previously noted constraint characterizing the non-decrease of tax revenues to the consolidated budget of the Russian Federation should be applied to the equation of social function maximization.

Thus, the theoretical macroeconomic model of individual taxation system is as follows (formula 11):

(11) (11)

The constraints of the system are as follows (formula 12):

(12)

Having all the values of equations' parameters, it is possible to determine the key parameters of individual taxation system using the method of simplex-tables transformation. We have proposed a number of areas for improving the taxation of individuals for the successful implementation of the described functions (Table 3).

Table 3. Proposed projects within the framework of personal income tax system

|

№

|

Project Name

|

Project Type

|

Project achievement ground

|

Tax instruments, projects, ground

(New and subjects to change are highlighted by italic)

|

|

1

|

Tax support of young and large families

|

In-system

|

1. Russian Federation Presidential Decree dated on 7th May of 2018 # 204 “About Russian Federation national targets and strategic tasks for the period up to 2024” (point 3).

2. President’s message to the Federal Assembly for the year 2022.

|

1. Cost deduction 5(7) square meters of individual property tax in case if the property (facility) is not used for business activity.

2. Exemption from personal income tax of revenue received by immovable property disposal for expansion of living space.

3. Exemption from 600 square meters area land tax for large families in case if the area is not used for business activity.

4. Exemption of one passenger car taxation registered on any of family’s member.

5. Standard tax deduction for children (with its amount increasing up to the region child living wage by applying region correction factors and limitations due to income rate).

6. Exemption from personal income tax of revenue received by means of families with children state support measures in accordance with Federal law “About families with children state support measures…”.

|

|

2

|

Tax stimulation of human resources investments

|

Intersystem

|

1. Russian Federation Presidential Decree dated on 7th May of 2018 # 204 of “About Russian Federation national targets and strategic tasks for the period up to 2024” (points 5, 9).

2. Russian Federation Presidential Decree dated 15th May of 2017 # 208 “About strategy of the Russian Federation economic security for the period up to 2030” (point 15 sub-paragraph 8, point 23).

3. Russian Federation Presidential Decree dated 01/12/2016, # 642 “About strategy of Russian Federation scientific and technological development” (point 29).

4. National program “Russian Federation digital economy”

(Approved by Presidium of the Russian Federation Presidential Council for Strategic Development and National projects, minutes of the meeting, dated 04/06/2019, # 7)

|

1. Social tax deductions for expenses on own education, education of children, siblings (with limitation depending on income level, removal of limitation according to the children’s age, level of education and establishing the possibility of unused balance of the deduction transfer to the next period).

2. Social tax deduction for expenses on voluntary pension insurance and provision.

3. Social tax deduction for expenses on own treatment, and treatment of parents and children (with increasing of age criterion up to 24 years old during full-time studying period)

4. Social tax deduction forexpenses on passing an independent qualification assessment.

5. Exemption from personal income tax of expenses on studying educational programs in licensed organizations; expenses on passing an independent qualification assessment; income in the form of travel cost reimbursement to the places of education and back for the persons studying in the Russian preschool institutions having correspondent license and not reached 18 years old.

|

|

3

|

Tax regulation of poverty and social inequality

|

In-system

|

1. Russian Federation Presidential Decree dated 15th May of 2017 # 208 “About strategy of the Russian Federation economic security for the period up to 2030” (point 14 sub-paragraph 6, point 23, sub-paragraph 5).

2. President’s message to the Federal Assembly for the year 2022.

|

1. Possible establishment of a non-taxable (free) minimum in case of an increase of personal tax income base rate up to 15%.

2. State benefits and compensations personal income tax exemption (except compensation for unused vocation).

3. Double standard child tax deduction for single parents.

4. Tax exemption from fixed deduction for natural persons’ properties (in square meters and for amounts up to 100,000 rubles) in case the property (facility) is not used for business activity.

5. Taxpayer’s personal income tax standard deduction for particular categories of individuals who are limited in the possibility to obtain labor income (disabled persons of the 1st and 2nd groups, disabled since childhood) (while increasing the amount of their provision up to the level of the working population living wage in the region).

6. For particular categories of persons who are limited of possibility to obtain labor income (disabled persons of the 1st and 2nd groups, disabled since childhood) exemption from land tax of 600 square meters floor space, and also exemption from Property tax of natural person for one subject of each type in case if the property (facility) is not used for business activity.

7. Exemption from personal income tax for revenue received in the form of charitable assistance by orphaned children, children left without parental care, and children of families whose revenue for one member does not exceed the regional living wage.

8. Establishment of land tax rate of 0,6% regarding the land occupied by housing stock, personal subsidiary plots, and allocated in urban areas.

|

|

4

|

Intensification of natural person investment activity

|

In-system

|

1. Russian Federation Presidential Decree dated 15th May of 2017 # 208 “About strategy of the Russian Federation economic security for the period up to 2030” (point 16 sub-paragraph 2, point 19 sub-paragraph 5).

|

1. Investment tax deduction

(type A deduction is provided only while actual execution of a transaction on an individual investment account)

2. Tax deduction for carried forward losses because of transactions with securities and operations with derivative financial instruments.

3. Tax deduction for carried forward losses because of participation in an investment partnership.

4. Exemption from personal income tax of some income range by dividends (point 84 article 217 Tax code of the Russian Federation) (temporary reduction of basic personal income tax rates on income in the form of dividends)

5. Exemption from personal income tax during 2022 and 2023 for revenue received from gold bullion sales.

6. Exemption from personal income tax of revenue received from the sale of shares in the authorized capital; revenue received from joint stock companies and other organizations; winnings of the operations of the state loans; incomes in the form of property received by a controlled person from CFC (controlled foreign company).

7. Fixed personal income tax for the revenue received from CFC.

|

|

5

|

Stimulation of individual entrepreneurial initiative

|

Intersystem

|

1. Russian Federation Presidential Decree dated 7th May of 2018 # 204 “About national goals and strategic tasks of the Russian Federation development for the period up to 2024” (point 13).

2. National project

“Small and medium business and support of the individual entrepreneurial initiative”

|

1. Professional income tax

(introduction of indexation for the income maximum amount in order to apply tax regime)

2. Professional tax deduction.

3. Exemption from personal income tax of the personal subsidiary plots’ members revenue range (tutoring etc.) and of the peasant farms.

4. Introduction of personal income tax holidays for self-employed persons on the general taxation system when setting the limit of taxable income.

|

|

6

|

Improvement of the housing condition quality

|

In-system

|

1. Russian Federation Presidential Decree dated 7th May of 2018 # 204 “About national goals and strategic tasks of the Russian Federation development for the period up to 2024” (point 6).

2. National project

“Housing and urban environment”

(Approved by Presidium of the Russian Federation Presidential Council for Strategic Development and National projects, minutes of meeting, dated 24/12/2018, # 16)

|

1. Exemption from personal income tax of compensation for reimbursement of mortgage loan interest; revenue in the form of housing cost received free of charge in accordance with the legislation.

2. Exemption from personal income of revenue received by the sale of property, owned by a taxpayer for more than maximum established period 3 (5) years.

3. New mechanism of differentiated granting of the property tax deduction (table 4.1.3), creating the possibility to obtain property tax deductions for several mortgage loans (for an amount not more than 3 million rubles).

4. Property tax deduction for residential property rental costs.

5. Applying increasing coefficients to land tax for individual housing construction.

6. The possibility of applying a tax to professional income while renting out residential premises.

7. Reduction of the time-limit period for possession of single residential premises for personal income tax purposes.

|

Source: developed by the author.

Discussion

The system approach in taxation has been applied relatively recently. The application of the system approach in taxation ensures the realization of multidirectional interests of all participants of tax relations and is also relevant in the sphere of taxation management. In this case, the theoretical significance of the system approach the author concludes in the integrity and nature of the relationship of tax management elements, practical - in the multidirectional interests, goals, objectives of tax relations participants [27].

First, the present article contributes directly to the extensive literature on systems economics [28-30]. Secondly, there are no analogues of the presented architectonics of the taxation system, in particular it takes into account not only its internal and external environment, but also the mechanisms of transformation under the influence of evolutionary processes. Some of its elements in general do not contradict the results of foreign studies presented earlier. Thus, the selected principles of system construction correspond to the principles of a complex economic system highlighted by Roundy et al. [18]. Roundy: self-organization; open but clear boundaries; complex components; nonlinearity; adaptability and sensitivity to initial conditions. A single position coordinated with the author's position is also noted in foreign studies on the interaction between taxation of individuals and the system of social support [8].

A debatable point is the chosen methodological approach of the study. In the literature on public finance, there are two main approaches to the evaluation of tax system projects and policies [30]. One of them is normative and studies the optimal tax system, and it is used in the context of this paper. The other way examines the excess tax burden at a point defined by the existing tax system. A number of researchers confirm the priority of the second approach, as it has intuitive appeal and is widely used in policy making as a comparative measure of distortion from different taxes [31]. At the same time, the theory of optimal taxation (method one) aims to characterize which tax system should be chosen to maximize the social welfare function subject to a number of constraints. The optimality of a particular tax system depends on the choice of the social welfare function [32].

As for the type composition of taxes included in individual taxation system, it seems to be the most discussed in the scientific literature. In particular, the scientific community has reached a consensus on the issue of including taxes on income, property, and capital into the system of personal taxation. It has been found that residential taxation policy affects how capital income should be taxed, due to the substitution of residential and nonresidential capital [5]. Scholars give a special increasing role to inheritance and gift taxes [33]. At the same time, the position on indirect taxes is ambiguous. In contrast to the author's opinion, for example, Christl et al. (2020) believe that indirect taxes are an independent element of individual taxation system (the current study refers them to the external environment elements) [34]. They emphasize the importance of including both indirect taxes and in-kind benefits in a comprehensive analysis of the redistributive impact of the welfare state. Such an approach of American scientists is fraught with the fact that within the framework of the presented tax system architectonics, indirect taxes, being built into the system of regulators, should be established primarily in the interests of natural persons. However, such taxes are far from being business-neutral, and therefore should be built into the system of taxation of economic entities (organizations), while taking into account individual interests of individuals.

Conclusions

Scientific novelty of the study consists in forming the concept of architectonics of individual taxation system. Such system is a dual open unrestricted spatio-temporal economic system, consisting of lower level subsystems: object, project, process, and environment subsystems, differentiated by the following objectives. First, impact on the population (spatial impact) and the second, sustainable evolutionary development (temporal impact). This system has the property of parity and operates on the principles of permanence and stability, coordination, dynamism and synergy.

As noted above, the effective functioning of any system is possible only based on the principles of duality. Duality in the system context is understood as a situation in which there are two systems represented by elements and relations between them. Each element of one system is compared with an element of the other. Each relation on the set of elements of the first system is compared with a relation on the set of elements of the second system in such a way that if the elements of the first system are in a certain relation, then their corresponding elements of the second system are also in this relation [29].

The possibilities of practical application of the results of this study consist in the use of the presented architectonics of individual taxation system for the development of tax regulation instruments by governments and ministries of the world, as well as national tax administrations for the development of mechanisms of tax control over the income, property and capital of individuals.

The presented description of individual taxation system gives only its internal semantics, not revealing the peculiarities of functioning and building relationships in the external space. In this connection, the two most relevant areas for further research of the system approach in the taxation of individuals are as follows:

1) development of mathematical modeling of the system architectonics and transforming it from a general system view into a model that can be subjected to validation;

2) further clarification and identification of tax system elements to specify the legislative norms and rules for determining tax liabilities, the mechanism of their administration.

The implementation limitations of the study derive in part from its methodological limitations, since further testing of the mathematical model, as noted earlier, requires either a complete set of confidential data on taxpayers or a series of laboratory experiments followed by extrapolation of the sample results to the general population. In addition, the applicability of the presented model (as well as any other mathematical model) is limited by the degree of similarity between the model and the original. In particular, the author's development is based on the results of the tax policy in the Russian Federation. While adaptation of it in other countries would require additional parameter superstructure, for example, the transformation of the equation characterizing the regulatory function of taxes in terms of inclusion or exclusion of certain decile groups of the population by income.

Библиография

1. Леонтьев Б.Б. Обоснование теории системной экономики // Правовая информатика. 2015. №4. С. 4-21.

2. Алиев С.Б. Правовой мониторинг регулирования интеллектуальной собственности в Евразийском экономическом пространстве // Мониторинг правоприменения. 2015. №3 (16). С. 4-13.

3. Цокова В.А., Кабисова А.Р., Халин А.А. Методологические аспекты анализа сущности налоговой системы на основе системного подхода // Экономические исследования. 2013. № 1. С. 5.

4. Шмелев Ю.Д. Концепция реформирования налоговой системы Российской Федерации, основанная на реализации принципа справедливости и социальной функции налогов: дис. доктора экономических наук: 08.00.10 – Финансы, денежное обращение и кредит. Москва. 2008. 459 с.

5. Makoto Nakajima Capital income taxation with housing // Journal of Economic Dynamics and Control. 2020. Vol. 115. 103883. https://doi.org/10.1016/j.jedc.2020.103883.

6. Horne R., Felsenstein D. Is property assessment really essential for taxation? Evaluating the performance of an ‘Alternative Assessment’ method // Land Use Policy. 2010. Vol. 27. Is. 4. P. 1181-1189. https://doi.org/10.1016/j.landusepol.2010.03.008.

7. Morini M., Pellegrino S. Personal income tax reforms: A genetic algorithm approach // European Journal of Operational Research. 2018. Vol. 264. Is. 3. P. 994-1004. https://doi.org/10.1016/j.ejor.2016.07.059.

8. Benczúr P., Kátay G., Kiss Á. Assessing the economic and social impact of tax and benefit reforms: A general-equilibrium microsimulation approach applied to Hungary // Economic Modelling. 2018. Vol. 75. P. 441-457. https://doi.org/10.1016/j.econmod.2018.06.016.

9. Bhattarai K., Benjasak C. Growth and redistribution impacts of income taxes in the Thai Economy: A dynamic CGE analysis // The Journal of Economic Asymmetries. 2020. Vol. 23. https://doi.org/10.1016/j.jeca.2020.e00189.

10. Тихонова А.В. Имитационное математическое моделирование системы подоходного налогообложения с использованием критерия Q-Тьюки // Экономические и социальные перемены: факты, тенденции, прогноз. 2019. Т. 12. № 1. С. 138-152. DOI: 10.15838/esc.2019.1.61.8

11. Avram S., Popova D. Do taxes and transfers reduce gender income inequality? Evidence from eight European welfare states // Social Science Research. 2021. 102644. https://doi.org/10.1016/j.ssresearch.2021.102644.

12. Frey C., Christoph A. Schaltegger Progressive taxes and top income shares: A historical perspective on pre-and post-tax income concentration in Switzerland // Economics Letters 2016. Vol. 148. P. 5-9. https://doi.org/10.1016/j.econlet.2016.08.041.

13. Nicolis G., Prigogine I. Self-organization in nonequilibrium systems // Wiley, New York, NY. 1977.

14. Statistics on labour income and inequality. Режим доступа: https://ilostat.ilo.org/topics/labour-income/ (дата обращения: 05.09.2023).

15. Glogowsky U. Behavioral responses to inheritance and gift taxation: Evidence from Germany // Journal of Public Economics. 2021. Vol. 193. https://doi.org/10.1016/j.jpubeco.2020.104309.

16. Ксиропулос И.Д. Налоговые инструменты социальной поддержки населения / И.Д. Ксиропулос // Налоги и налогообложение. 2017. № 6. С. 43-57.

17. Клейнер Г.Б. Стратегия системной гармонизации экономики России // Экономические стратегии. 2008. № 5-6. С.72-79.

18. Roundy P.T., Bradshaw M., Beverly K. Brockman The emergence of entrepreneurial ecosystems: A complex adaptive systems approach // Journal of Business Research. 2018. Vol. 86. P. 1-10. https://doi.org/10.1016/j.jbusres.2018.01.032.

19. Najmaei A. Using mixed-methods designs to capture the essence of complexity in the entrepreneurship research: An introductory essay and a research agenda // E.S.C. Berger, A. Kuckertz (Eds.), Complexity in entrepreneurship, innovation and technology research. 2016. P. 13-36.

20. Fiss P.C. A set-theoretic approach to organizational configurations // Academy of Management Review. 2007. Vol. 32 (4). P. 1180-1198.

21. Berger E.S.C. Is qualitative comparative analysis an emerging method? Structured literature review and bibliometric analysis of QCA applications in business and management research // E.S.C. Berger, A. Kuckertz (Eds.), Complexity in entrepreneurship, innovation and technology research. 2016. P. 1-9.

22. Olya H.G., Mehran J. Modelling tourism expenditure using complexity theory // Journal of Business Research. 2017. Vol. 75 (2). P. 147-158.

23. McKelvey B. Toward a complexity science of entrepreneurship // Journal of Business Venturing. 2004. Vol. 19 (3). P. 313-341.

24. Graebner M.E., Martin J.A., Roundy P.T. Qualitative data: Cooking without a recipe // Strategic Organization. 2012. Vol. 10 (3). P. 276-284.

25. Милоголов Н.С., Пономарева К.А. Международная кооперация налоговых администраций при налогообложении цифровых бизнес-моделей: миф или реальность? // Налоги. 2021. № 3. С. 29-33.

26. Marenzi A., Rizzi D., Zanette M. Incentives for voluntary health insurance in a national health system: Evidence from Italy // Health Policy. 2021. Vol. 125. Is. 6. P. 685-692. https://doi.org/10.1016/j.healthpol.2021.03.007.

27. Тюрина Ю.Г. Теоретические аспекты применения системного подхода в налогообложении // Экономика. Налоги. Право. 2017. №2. С. 128-133.

28. Bertalanffy L. Stoffwechseltypen und Wachstumstypen, 61, Biol Zentralbt. 1941. P. 510-530.

29. Клейнер Г.Б. Принципы двойственности в свете системной экономической теории // Вопросы экономики. 2019. № 11. С. 127-149.

30. Quade E.S. Analysis for Military Decisions // United States air force project rent. 1964. 394 p.

31. Tran C., Wende S. On the marginal excess burden of taxation in an overlapping generations model // Journal of Macroeconomics. 2021. 103377. https://doi.org/10.1016/j.jmacro.2021.103377.

32. Fehr H., Kindermann F. Taxing capital along the transition-Not a bad idea after all? // J. Econom. Dynam. Control. 2015. Vol. 51. P. 64.

33. Kindermann F., Mayr L., Sachs D. Inheritance taxation and wealth effects on the labor supply of heirs // Journal of Public Economics. 2020. Vol. 191. 104127. https://doi.org/10.1016/j.jpubeco.2019.104127.

34. Christl M., Köppl–Turyna M., Lorenz H., Kucsera D. Redistribution within the tax-benefits system in Austria // Economic Analysis and Policy. 2020. Vol. 68. P. 250-264. https://doi.org/10.1016/j.eap.2020.09.011

References

1. Leontiev, B.B. (2015). Substantiation of the theory of system economy. Legal informatics, 4, 4-21.

2. Aliev, S.B. (2015). Legal monitoring of intellectual property regulation in the Eurasian Economic Space. Law enforcement monitoring, 3, 4-13.

3. Tsokova, V.A., Kabisova, A.R., & Khalin, A.A. (2013). Methodological aspects of the analysis of the essence of the tax system based on a systematic approach. Economic Research, 1, 5.

4. Shmelev, Y. D. (2008). The concept of reforming the tax system of the Russian Federation, based on the implementation of the principle of justice and the social function of taxes: dis. Doctor of Economic Sciences: 08.00.10-Finance, money circulation and credit. Moscow.

5. Nakajima, M. (2020). Capital income taxation with housing. Journal of Economic Dynamics and Control, 115, 103883. Retrieved from https://doi.org/10.1016/j.jedc.2020.103883.

6. Horne, R., & Felsenstei,n D. (2010). Is property assessment really essential for taxation? Evaluating the performance of an ‘Alternative Assessment’ method. Land Use Policy, 27(4), 1181-1189. Retrieved from https://doi.org/10.1016/j.landusepol.2010.03.008.

7. Morini, M., & Pellegrino, S. (2018). Personal income tax reforms: A genetic algorithm approach. European Journal of Operational Research, 264(3), 994-1004. Retrieved from https://doi.org/10.1016/j.ejor.2016.07.059

8. Benczúr, P., Kátay, G., & Kiss, Á. (2018). Assessing the economic and social impact of tax and benefit reforms: A general-equilibrium microsimulation approach applied to Hungary. Economic Modelling, 75, 441-457. Retrieved from https://doi.org/10.1016/j.econmod.2018.06.016.

9. Bhattarai, K., & Benjasak, C. (2020). Growth and redistribution impacts of income taxes in the Thai Economy: A dynamic CGE analysis. The Journal of Economic Asymmetries, 23. Retrieved from https://doi.org/10.1016/j.jeca.2020.e00189

10. Tikhonova, A.V. (2019). Simulation mathematical modeling of the system of income taxation using the Tukey Q criterion. Economic and social changes: facts, trends, forecast, 12, 1, 138-152. doi:10.15838/esc.2019.1.61.8

11. Avram, S., & Popova, D. (2021). Do taxes and transfers reduce gender income inequality? Evidence from eight European welfare states. Social Science Research, 102644. Retrieved from https://doi.org/10.1016/j.ssresearch.2021.102644

12. Frey, C., & Christoph, A. (2016). Schaltegger Progressive taxes and top income shares: A historical perspective on pre-and post-tax income concentration in Switzerland. Economics Letters, 148, 5-9. Retrieved from https://doi.org/10.1016/j.econlet.2016.08.041

13. Nicolis, G., & Prigogine, I. (1977). Self-organization in nonequilibrium systems. Wiley, New York, NY.

14. Statistics on labour income and inequality. Retrieved from https://ilostat.ilo.org/topics/labour-income/

15. Glogowsky, U. (2021). Behavioral responses to inheritance and gift taxation: Evidence from Germany. Journal of Public Economics, 193. Retrieved from https://doi.org/10.1016/j.jpubeco.2020.104309

16. Xiropoulos, I.D. (2017). Tax instruments of social support of the population. Taxes and taxation, 6, 43-57.

17. Kleiner, G.B. (2008). Strategy for Systemic Harmonization of the Russian Economy. Economic Strategies, 5-6, 72-79.

18. Roundy, P.T., Bradshaw, M., Beverly, K., & Brockman (2018). The emergence of entrepreneurial ecosystems: A complex adaptive systems approach. Journal of Business Research, 86, 1-10. Retrieved from https://doi.org/10.1016/j.jbusres.2018.01.032.

19. Najmaei, A. (2016). Using mixed-methods designs to capture the essence of complexity in the entrepreneurship research: An introductory essay and a research agenda. Complexity in entrepreneurship, innovation and technology research, 13-36.

20. Fiss, P.C. (2007). A set-theoretic approach to organizational configurations. Academy of Management Review, 32(4), 1180-1198.

21. Berger, E.S.C. (2016). Is qualitative comparative analysis an emerging method? Structured literature review and bibliometric analysis of QCA applications in business and management research. Complexity in entrepreneurship, innovation and technology research, 1-9.

22. Olya, H.G., & Mehran, J. (2017). Modelling tourism expenditure using complexity theory. Journal of Business Research, 75(2),147-158.

23. McKelvey, B. (2004). Toward a complexity science of entrepreneurship. Journal of Business Venturing, 19(3), 313-341.

24. Graebner, M.E., Martin, J.A., & Roundy, P.T. (2012). Qualitative data: Cooking without a recipe. Strategic Organization, 10(3), 276-284.

25. Milogolov, N.S., & Ponomareva, K.A. (2021). International cooperation of tax administrations in the taxation of digital business models: myth or reality? Taxes, 3, 29-33.

26. Marenzi, A., Rizzi, D., Zanette, M. (2021). Incentives for voluntary health insurance in a national health system: Evidence from Italy. Health Policy, 125(6), 685-692. Retrieved from https://doi.org/10.1016/j.healthpol.2021.03.007

27. Tyurina, Yu.G. (2017). Theoretical aspects of applying a systematic approach to taxation. Economy. Taxes. Right, 2, 128-133.

28. Bertalanffy, L. (1941). Stoffwechseltypen und Wachstumstypen. Biol Zentralbt, 510-530.

29. Kleiner, G.B. (2019). Principles of duality in the light of systemic economic theory. Questions of Economics, 11, 127-149.

30. Quade, E.S. (1964). Analysis for Military Decisions. United States air force project rent, 394.

31. Tran, C., & Wende, S. (2021). On the marginal excess burden of taxation in an overlapping generations model. Journal of Macroeconomics, 103377. Retrieved from https://doi.org/10.1016/j.jmacro.2021.103377

32. Fehr, H., & Kindermann, F. (2015). Taxing capital along the transition-Not a bad idea after all? J. Econom. Dynam. Control, 51, 64.

33. Kindermann, F., Mayr, L., & Sachs, D. (2020). Inheritance taxation and wealth effects on the labor supply of heirs. Journal of Public Economics, 191, 104-127. Retrieved from https://doi.org/10.1016/j.jpubeco.2019.104127

34. Christl, M., Köppl–Turyna, M., Lorenz, H., & Kucsera, D. (2020). Redistribution within the tax-benefits system in Austria. Economic Analysis and Policy, 68, 250-264. Retrieved from https://doi.org/10.1016/j.eap.2020.09.011

Результаты процедуры рецензирования статьи

В связи с политикой двойного слепого рецензирования личность рецензента не раскрывается.

Со списком рецензентов издательства можно ознакомиться здесь.

Предмет исследования. Предметом исследования выступают отношения, возникающие в процессе налогового администрирования физических лиц.

Методология исследования, использованная автором, основана на следующих методах научного познания: сравнение, анализ, синтез теоретического материала.

Актуальность. Тема, предложенная автором, представляется весьма актуальной. В первую очередь, это обусловлено тем, что грамотно выстроенная система налогообложения физических лиц позволяет решать в том числе и социальные задачи.

Научная новизна. Научная составляющая исследования заключается в модернизации существующей системы налогообложения физических лиц, а также обоснованию применения системного подхода к моделированию основных элементов такой системы.

Библиография. Анализ библиографии позволяет сделать вывод о том, что автор в достаточном объеме изучил научные труды по исследуемой проблематике. Присутствуют иностранные источники, в целом список литературы состоит из 34 наименований.

Апелляция к оппонентам. В статье присутствуют адресные ссылки на исследования, в том числе иностранные, дана их критическая оценка.

Стиль, структура, содержание. Стиль статьи является научным, соответствует требованиям журнала. В статье выделены классические структурные разделы. Устоявшиеся налоговые категории верно переведены на английский язык.

Автор на хорошем теоретическом уровне проводит анализ структурных сдвигов денежных доходов в России. Особое внимание уделено обоснованию необходимости трансформации существующей системы налогообложения физических лиц. Интерес вызывает авторская структура системы налогообложения физических лиц и входящих в нее элементов – подсистем. В статье проведено исследование дуалистичности системы налогообложения физических лиц, обоснована ее взаимосвязь с социальной политикой. Дискуссионным является предложение автора освободить от налогообложения один автомобиль на семью, в первую очередь, с точки зрения оценки эффективности такого нововведения для бюджетной системы. Какова будет доля выпадающих доходов? Предложения автора по развитию существующей системы налогообложения физических лиц являются интересными, однако, требуют дополнительного обоснования, что вероятнее всего будет отражено в следующих публикациях.

В качестве замечаний- рекомендаций хотелось бы отметить следующее.

Под рисунком 1 следует сделать ссылку на источник, если он составлен лично автором, то необходимо указать это. Данные в таблицах необходимо обновить по состоянию на 2022 год или объяснить, почему такие данные не могут использоваться.

Выводы, интерес читательской аудитории. Представленный материал может открыть новые перспективы для дальнейших исследований. Он будет интересен тем, кто занимается изучением проблем налогового администрирования и моделирования системы налогообложения физических лиц.

Статья соответствует требованиям журнала «Налоги и налогообложение», предъявляемым к такого рода работам, и рекомендуется к публикации с учетом замечаний рецензента.

|