|

DOI: 10.7256/2454-0765.2018.2.28268

Дата направления статьи в редакцию:

05-12-2018

Дата публикации:

15-02-2019

Аннотация:

Цель исследования имеет эксплораторный характер. Предметом исследования является рыночная стоимость акционерного капитала российских корпораций. Авторы подробно рассматривают аспект влияния сруктуры собственников, а именно, присутствие государства в числе акционеров компаний на изменение их рыночной стоимости. Авторы отвечают на вопрос каким образом инвесторы в России воспринимают сам факт, а таже степень присутствия государства в числе собственников компаний. В основе темы исследования лежит концепция рыночной эффективности (Фама, 1998). В основе анализа лежит производная модели оценки рыночной стоимости компаний Олсона (1995). Она представляет собой уравнение регрессии где в качестве зависимой переменной выступает рыночная стоимость компании, а независимых - балансовая стоимость собственного капитала, величина прибыли, структура собственности. Основными выводами проведенного исследования являются: данные в целом по рынку показывают отсутствие однозначной реакции на факт государственного присутствия в структуре собственников, однако в разрезе отраслей наблюдаются значительные расхождения. Так, по результатам исследования, увеличение государственного присутствия приветстуется инвесторами в сферах транспорта, торговли и кредита. Отрицательная реакция присутствует в сферах добывающей промышленности и металлообработки. Различия оъясняются разными ожиданиями эффекта государственного присутствия в отраслях.

Ключевые слова:

государственное участие, рыночная стоимость, влияние на стоимость, собственный капитал компании, финансовый рынок, финансовая отчетность, эффективный рынок, отрасль промышленности, инвестор, рынок ценных бумаг

Abstract: The impact of government ownership of a firm’s equity has been a topic of heated debate in finance, economics, and politics. The extant literature provides evidence of both positive and negative effect of government ownership on the market value of firms with multiple reasons in favor of both effects. There has also been research on how such effects may differ in different markets. This paper aims to explore the value-relevance of such in the financial market of Russia. We are using a sample of 159 Russian listed companies to identify the relationship between market value and government ownership of equity. Even though the previous studies support a positive relationship between the two variables the evidence from Russian listed firms proves otherwise. We find that the Russian market does not reward governmental control, however, it doesn’t penalize it as well. The research connects to the efficient market hypothesis (EMH).

Keywords: government ownership, maket value, value relevance, firm's equity, financial market, financial peformance, efficient maket, industry sector, investor, stock exchange

Introduction

The structure of ownership of firm equity has been widely discussed as a factor generating both positive and negative influences on various aspects of a firm performance. Two main streams of literature exist in this relation, the most popular one being the one exploring various effects government ownership of a firm’s equity exerts on its financial performance and the less significant in volume however not least interesting being the stream on the direct market value relevance of the government control. Both literatures hold in common the view that governmental ownership can have both positive and negative effects on either one of the performance indicators. Our research contributes to the latter and dwells upon the efficient market hypothesis (EMH) (Fama, 1998) supporting that the current market value of the firm’s equity contains the publicly available data on the equity structure as well as other information, meaning that investors making decisions as to purchase a particular share of stock will keep in mind all this information, thus knowing about the fact and degree of state-control over a firm and expressing their attitude towards it.

We are exploring the relationship between government ownership of a firm’s equity on its market value in Russia with the view of answering the research question of how investors in Russia perceive the fact and degree of government ownership on equity measured through the market value of equity. Carney and Child (2013) report a growing role of government in equity ownership in East Asian countries between 1996 and 2008. Boubakri, Ghoul, Guedhami and Meggisnson (2017) report that in emerging markets SOEs account for 28% of the largest companies. However an interesting tendency is transpiring, despite of an active privatization in both developed (mostly Europe) and developing markets (Asian countries, East Europe, Latin America) the share of state-controlled companies continues to grow, but a more active phase of this growth has primarily happened in the period after the financial crisis, when the government ownership started to be associated with a bailout strategy and certain references in receiving support (Guedhami, 2012; Nash, 2017).

Another peculiarity is observed now with regard to government ownership of firms’ equity, some companies were formed as a result of privatization of SOE’s capital and the government held on to a proportion of equity (usually around 50% as reported by Tran, Nonneman & Jorrisen, 2014), having become a shareholder, in other cases the ownership was obtained by simply purchasing a share of equity in the market, the result being seen in the form of low percentage of government ownership of the firm’s equity. Such a form of acquisition was reported by Eckel and Vermaelen (1986) for North American firms. Thus, the trend reported by the extant research shows the proliferation of the latter form of acquisition in the period after the financial crisis in Europe and Asia, apparently in the response to the crisis effects, with some evidence in favor of a more positive perception of such a type by investors, but again the findings differ depending on economy (Huang & Xiao, 2012) and firm size (Truong et al., 2006).

Our research is of exploratory nature and is attempting to explore the nature of relationship between government ownership and market value for Russian listed firms. We are using the evidence from a sample of 159 publicly traded firms listed in the stock exchange of Russia found in Bloomberg database.

Literature review

The extant literature abounds in research on value relevance of various engagements of the firms, including financial and non-financial information with the main theoretical concept being the efficient market hypothesis (EMH) (Fama, 1970; Kendall, 1958; Fama, 1998) stating that share prices contain all publicly available information, including the information on the public ownership of the firm’s equity.

However the research on the impact of government ownership on market value doesn’t have an extensive history. The object of such a consideration is a mixed enterprise, defined by Spenser (1959) as the one which is owned jointly by public and private management. Such a form of ownership is described to be occurring as the result of either a state-owned enterprise (SOEs) being privatized but government still retains its stake, or the state acquires the shares of a private jointly owned enterprise.

The first comprehensive inquiry into the effect of state ownership on the market value of a firm was made by Eckel and Vermaelen (1986), who reported both negative and positive impact, the positive including expectation of lower risk and access to subsidy, synergistic effects; the negative ones being lower expected profitability capitalizing into share prices. However the authors also connect the research to the conceptual framework of agency problem and Jensen and Meckling’s (1976) perception of alignment of agents’ interest with the principals’ ones, but that depended on the degree of regulation.

Since then there has been two parallel streams of literature exploring the effects of public ownership: market value relevance effects and the financial performance effects, however the results of both streams are linked by the overarching concept of EMH. It has to be noted that significantly less studies found purely positive effects of state involvement (Jiang et al., 2008; Liao and Young, 2012), and more studies identified various either negative (Sappington and Stiglitz, 1987; Shleifer and Vishny, 1994; Boycko et al., 1996) or mixed (Wei et al., 2005; Hess et al., 2010; Alfaraih, Alanezi, & Almujamed, 2012) effects. The main reasons for negative effects listed as the agency conflict and the positive impact caused mainly by lower risk perception. It has also been found that in transition economies the effects might be different (Huang & Xiao, 2012).

The most interesting explanation provided by the current literatures is the one contrasting the ‘helping hand’ with the ‘grabbing hand’ of the government, which might take advantage of its controlling position and abuse the earnings (Sappington and Stiglitz, 1987).

We will connect to the stream of literature of purely market effects of governmental ownership, examining the latter as an independent variable in market valuation (Alfaraih, Alanezi, & Almujamed, 2012; Razak, Saidi, & Mahat, 2013) in the widely used valuation model by Ohlson (1995), which and become a conventional tool in measuring certain value effects (Ohlson, 1995; Hassel, 2005; Loh et al. 2017).

Our goal is to explore the effect of government ownership of firm equity in Russia. To reach the goal we have developed two hypotheses.

Hypothesis 1 (H1): Firms that have certain degree of government ownership have lower market values than privately owned firms.

H1 explores the market value relevance of the fact of government control, connecting to the EMH and previous research supporting the expectation of agency conflict (Eckel & Vermaelen, 1986) and the ‘grabbing hand’ effect by the investor (Huang & Xiao, 2012) .

Hypothesis 2 (H2): Firms with higher degree of government ownership have lower market value values than firms with lesser degree of government control.

H2 connects to the concept of ultimate control (Wang & Xiao, 2009) where the degree of government control is ranging between 0 and 100% and the assumption that less state control translates into better performance of firms in terms of profitability and productivity (Tran et al., 2014).

Data and Methods

The empirical analysis relies on a sample of 159 firms out of the target population of the 260 corporations listed in the Russian financial market. We use the data derived from the Bloomberg database including those on government ownership, market value, and other variables. Data analysis is done with the help of statistical software IBM SPSS and the R.

In this study, we are using a derivation of the seminal Ohlson’s (1995) model of a firm market value relation to accounting data and other information. In finance and accounting research Ohlson’s valuation model is viewed as a conventional tool in determining value-relevance of various data (Hassel, 2005; Loh et al, 2017; Lourenco & Eugenio, 2011).

The model is using a regression tool to determine the nature of relationship between variables and the impact of independent variables on the intercept. As long as the data on market value is usually very heterogeneous we are using the weighted least squares regression method. Our model derivation is based on the method used by Loh and Thomas (2017) with our modifications in terms of ownership variable. We will test several specifications of the model with the baseline having the following shape:

MVi,t+4 = α0 + α1BVi,t + α2EARNi,t + α3EARNi,t × NEGi,t + εi,t , (1)

In the model MVi,t+4 is the market value four months after financial year-end of company i; BVi,t is the book value of common equity at the year-end of company i; EARNi,t is earnings before extraordinary items at the year-end of company i; NEGi,t is a dummy variable equal to 1 if at the t year end the firm had losses and 0 if otherwise, and εi,t is the error term. We are including the book value and earnings, because in line with the previous research (Loh et al. 2017; Hassel, 2005; Ohlson, 1995) book value shows a positive relationship with the market value, earnings, in contrast, can show a negative relationship with the market value, because profit is usually rewarded by the market and loss is usually penalized (V. Brecht et al., 2018). First we run it as Model (1) and test its specifications.

As the next step we will include the ownership variable first as a dummy variable, with 0 – if the firm had no state ownership and 1 – if there was some degree of it (dummy variable OWNi,t), to find the link between the ownership and the market value to accept/reject the hypothesis H1 (Model 2). To test the hypothesis 2 (H2) we explore the relationship between the degree of government ownership and the market value replacing the dummy variable OWNi,t with a continuous variable, the share of equity owned by the government (between 0 and 100%) and produce the model (3). After that we will generate the model 4, the one containing a control variable, for the control variable we chose to use the firms belonging to service or manufacturing sector, the INDit variable, which we assign the value – “0” if its service and “1” if the company works in manufacturing sector.

Assessing the model specification and predicting power we will examine the R² for the three models and the p-values for the significance of the relationships, we are expecting to see a value of determination coefficient of more than 0.5, which would mean that the model can predict 50% of the variance of market value by the change in book value, earnings and profit/loss (model 1), we expect the value of R² to remain relatively constant for subsequent model specifications, at the significance level of p below 0.05. Therefore if the association proves to be statistically significant (p-value below 0.05) we will accept that the association did not happen by chance; if otherwise, we will accept the null hypothesis (no significant relationship).

Findings

1019 firms in total are listed in the Russian financial market, however out of those firms only 260 are active and report financials. And only 159 of the active 260 firms have enough values reported for the analysis. The selected 159 firms are characterized by high market values, have varied earnings and mostly larger book values of equity. The distribution of firms by main variables is positively skewed with a number of large outliers.

Table 1 summarizes the summary statistics of all variable used in this research describing the central tendency and the dispersion of variables used in the model.

Table 1. Summary statistics of variables

|

|

N

|

Minimum

|

Maximum

|

Mean

|

Std. Deviation

|

|

MV (Mln. RUB)

|

159

|

-4964.4

|

2823929.3

|

570390.1

|

2618195.2

|

|

EARN (Mln. RUB)

|

159

|

-405551

|

1022376

|

31185.9

|

133187.1

|

|

OWN

|

159

|

0

|

99.997

|

19.65

|

35.199

|

|

BV (Mln. RUB)

|

159

|

-284833

|

12015481.4

|

248861.8

|

1123554.4

|

Absolute values are shown in RUB, the mean value of earnings before extraordinary items for the sample was 31185.9 million RUB and the mean book value was almost 25 billion RUB, the mean market value for Russian listed companies was 570 trillion RUB. The government ownership in the sample ranged between 0% and almost 100 % with the mean value of 19.65%, which is quite high. However, only 58 firms out of the 159 (36.5%) had some degree of government control with the mean value of 53.9%. The distribution is bimodally shaped with more than 70% of the firms having the degree of government control between 0 and 10%.

Table 2. Correlation matrix of the variables

|

|

IND

|

MV

|

EARNNEG

|

EARN

|

BV

|

OWN%

|

OWNd

|

|

IND

|

1

|

-0.098

|

0.114

|

0.111

|

0.099

|

.175*

|

.178*

|

|

MV

|

|

1

|

-0.017

|

.680**

|

.505**

|

.244**

|

.217**

|

|

EARNNEG

|

|

|

1

|

.272**

|

0.042

|

0.048

|

0.067

|

|

EARN

|

|

|

|

1

|

.902**

|

.279**

|

.306**

|

|

BV

|

|

|

|

|

1

|

.262**

|

.264**

|

|

OWN%

|

|

|

|

|

|

1

|

.739**

|

|

OWND

|

|

|

|

|

|

.739**

|

1

|

|

*. Correlation is significant at the 0.05 level (2-tailed).

|

|

**. Correlation is significant at the 0.01 level (2-tailed).

|

From the correlation matrix (Pearson correlations) we can see a high value of correlation coefficient between earnings and book value (0.9 at a high significance level), we explain that by the simple pattern that firms having high book value of equity will be larger and have higher value of sales, such correlation is common for all markets, we will control the model for multicollinearity with variance inflation factors (VIFs). Among other peculiarities we can point out high significance of association between market value and the main independent variables of the model, however our model is using the weighted method so we cannot rely on the significances shown by Pearson values.

Table 3. Model 1 Regression Results

|

|

Unstandardized Coefficients

|

Standardized Coefficients

|

Collinearity Statistics

|

|

B

|

Std. Error

|

Beta

|

t

|

Sig.

|

Tolerance

|

VIF

|

|

BV

|

.751

|

.438

|

.184

|

1.712

|

.049

|

.389

|

2.570

|

|

Earn

|

18.407

|

5.287

|

.726

|

3.481

|

.001

|

.103

|

9.703

|

|

earnneg

|

-23.544

|

5.546

|

-.792

|

-4.245

|

.000

|

.129

|

7.759

|

|

R²

|

0.305

|

|

|

|

|

|

|

The first regression showed that the selected model has a good for predicting the variance of the intercept, the market value, with the R² higher than 0.3 and all independent variables showing statistically significant relationships with the market value at the p-values of less than 0.05. We conclude that our model has a good fit, but there are unobserved factors influencing the intercept. Thus we need to test other models.

Table 4. Model 2 Regression Results

|

Model 2

|

Standardized Coefficients

|

Collinearity control

|

|

Beta

|

t

|

p-value

|

t

|

VIF

|

|

BV

|

.793

|

.443

|

.194

|

1.788

|

.046

|

.382

|

2.619

|

|

EARN

|

18.569

|

5.301

|

.733

|

3.503

|

.001

|

.103

|

9.722

|

|

EARNNEG

|

-23.734

|

5.562

|

-.798

|

-4.267

|

.000

|

.129

|

7.778

|

|

OWNdum

|

-112952191148.399

|

162021923420.974

|

-.049

|

-.697

|

.487

|

.928

|

1.077

|

|

R Squared

|

0.307

|

|

|

Having included the factor of ownership (as a dummy variable) into the model we find that the fact of government ownership of the firm’s equity may have a slightly negative impact on the market value, however we need to reject such an association because the level of significance (p-value of 0.487) doesn’t allow us to admit that such an association did not happen by chance. Thus, we accept the null hypothesis. So, H1 does not hold for our sample.

Table 5. Model 3 Regression Results

|

Model 3

|

Standardized Coefficients

|

Collinearity control

|

|

Beta

|

t

|

p-value

|

t

|

VIF

|

|

BV

|

.810

|

.444

|

.198

|

1.823

|

.050

|

.380

|

2.634

|

|

earn

|

18.533

|

5.294

|

.731

|

3.501

|

.001

|

.103

|

9.710

|

|

earnneg

|

-23.706

|

5.554

|

-.797

|

-4.268

|

.000

|

.129

|

7.768

|

|

OWN%

|

-2044356010.266

|

2384419998.191

|

-.060

|

-.857

|

.393

|

.923

|

1.083

|

|

R Squared

|

0.308

|

|

|

Having replaced the dummy variable – government ownership with a continuous one we again do not find any statistically significant relationship between the degree of ownership and the firm value (the p-value 0.393), we can still see a high impact of book value and earnings on market value, but still government ownership does not produce any significant effect. However the significance of this association has increased with the change of variable from p-value of 0.487 to 0.393, however we cannot accept or reject the hypothesis 2 (H2) under these conditions as well.

As the next step, we want to test the model specification, we can see a large impact of unobservable factors which we will try to identify.

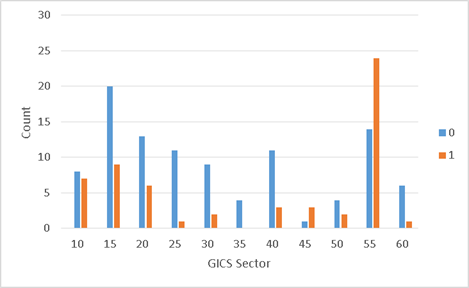

Observing the data we find a patent in government ownership by industry sector (Table 6). The highest concentration of government ownership we find in the oil, energy and web-design sectors; the smallest concentration is in software developing sector.

Table 6. Cross-tabulation of Industry and Ownership

|

|

Government Ownership by count

|

Total

|

Ownership %

|

|

GICS Sector

|

Oil

|

8

|

7

|

15

|

46.67%

|

|

Mining & Metals

|

20

|

9

|

29

|

31.03%

|

|

Transport

|

13

|

6

|

19

|

31.58%

|

|

Automobile

|

11

|

1

|

12

|

8.33%

|

|

Retail

|

9

|

2

|

11

|

18.18%

|

|

Software

|

4

|

0

|

4

|

0.00%

|

|

Banking

|

11

|

3

|

14

|

21.43%

|

|

Web

|

1

|

3

|

4

|

75.00%

|

|

Telecom

|

4

|

2

|

6

|

33.33%

|

|

Energy

|

14

|

24

|

38

|

63.16%

|

|

Investment

|

6

|

1

|

7

|

14.29%

|

|

Total

|

101

|

58

|

159

|

|

Fig. - 1 Distribution of ownership by sector[1]

To check how the sector can affect the market value we will include the variable into the model as a dummy, with “0” assigned to the service sectors and “1” – to manufacturing.

Table 7. Correlation matrix including the industry factor

|

|

IND

|

MV

|

EARNNEG

|

EARN

|

BV

|

OWN%

|

OWNd

|

|

IND

|

1

|

-0.098

|

0.114

|

0.111

|

0.099

|

.175*

|

.178*

|

|

MV

|

|

1

|

-0.017

|

.680**

|

.505**

|

.244**

|

.217**

|

|

EARNNEG

|

|

|

1

|

.272**

|

0.042

|

0.048

|

0.067

|

|

EARN

|

|

|

|

1

|

.902**

|

.279**

|

.306**

|

|

BV

|

|

|

|

|

1

|

.262**

|

.264**

|

|

OWN%

|

|

|

|

|

|

1

|

.739**

|

|

OWND

|

|

|

|

|

|

.739**

|

1

|

|

*. Correlation is significant at the 0.05 level (2-tailed).

|

|

**. Correlation is significant at the 0.01 level (2-tailed).

|

Regression of both models with the industry variable (Model 4 and Model 5) shows a significant increase in the determination coefficient value, which means a better fit of the model, also the p-values of the variables have significantly improved, however the VIF for the variable EARN reached critical proportions, which means there is more collinearity between market value and earnings depending on the industry.

Table 8. Model 4 Regression Results

|

Model 4

|

Standardized Coefficients

|

Collinearity control

|

|

Beta

|

t

|

p-value

|

t

|

VIF

|

|

BV

|

1.307

|

.474

|

.320

|

2.756

|

.007

|

.320

|

3.120

|

|

earn

|

11.858

|

5.757

|

.468

|

2.060

|

.041

|

.084

|

11.938

|

|

earnneg

|

-16.599

|

6.056

|

-.558

|

-2.741

|

.007

|

.104

|

9.598

|

|

OWNdum

|

-128641297806.8

|

158903061213.5

|

-.055

|

-.810

|

.419

|

.927

|

1.079

|

|

IND

|

-91441972514.0

|

33802223268.7

|

-.199

|

-2.705

|

.008

|

.797

|

1.254

|

|

R Squared

|

0.339

|

|

|

Table 9. Model 5 Regression Results

|

Model 5

|

Standardized Coefficients

|

Collinearity control

|

|

Beta

|

t

|

p-value

|

t

|

VIF

|

|

BV

|

1.325

|

.475

|

.324

|

2.789

|

.006

|

.319

|

3.136

|

|

earn

|

11.806

|

5.751

|

.466

|

2.053

|

.042

|

.084

|

11.932

|

|

earnneg

|

-16.555

|

6.049

|

-.557

|

-2.737

|

.007

|

.104

|

9.593

|

|

IND

|

-91523929612.8

|

33768164183.866

|

-.199

|

-2.710

|

.007

|

.797

|

1.254

|

|

OWN%

|

-2254663460.9

|

2338047178.740

|

-.066

|

-.964

|

.336

|

.922

|

1.084

|

|

R Squared

|

0.340

|

|

|

Therefore, including the control variable proved to be efficient for the model fit, the predicting power increased to 0.34, we conclude that belonging to the to the service sector has a significant effect on the market value. So we conclude that the IND variable improves the overall fir of the model. However he significance values of even though improved still haven’t reached the level of significance, we cannot reject the null hypothesis.

Discussion

In the course of our analysis we had to reject any impact of government ownership on firm value, neither the fact nor the degree of government ownership affects the market value of a firm in any way, the relationship may seem even negative, thus it may seem that the state control is penalized by the market, but such an association hasn’t been proved by this research.

However, as long as we discovered a significant impact from the industry factor we need to explore that question in further detail. For that, we broke the sample into industry-based groups and tried to evaluate the impact of government ownership in the groups with a sufficient number of cases to do a regression analysis (more than 25, more than 5 observations per variable).

The sectors identified as suitable for such an analysis are mining and metals, transportation and banking.

Mining

Variance of the market value in the mining sector can be predicted with a high certainty (determination coefficient of 0.94 and p-values below 0.05) with earnings, book value and the degree of government ownership. The sector sample is fairly homogenous and normally distributed, and no significant collinearity was detected, so we used a minimal least squares method (Table 10).

Table 10. Regression Results for mining and metals

| |

Standardized Coefficients

|

|

Beta

|

t

|

p-value

|

|

EARN

|

16.485

|

.975

|

1.404

|

16.913

|

.000

|

|

BV

|

-1.127

|

.206

|

-.363

|

-5.461

|

.000

|

|

OWN%

|

-6502049224.706

|

1406264686.241

|

-.413

|

-4.624

|

.000

|

|

EARNNEG

|

15.846

|

35.909

|

1.347

|

.441

|

.663

|

|

R Squared

|

0.939

|

Government ownership is significant and had a strong negative impact on market value (beta-value of -0.413). The result means that the market largely penalizes government ownership in mining anf metals sector, which we explain by the expectation of the ‘grabbing hand’ effect, with government abusing the rents generated by the sector.

Banking

Using the same model specification we can predict up to 99% of the variance in the market value in the banking sector (Table 11).

Table 11. Regression Results for Banking

| |

Standardized Coefficients

|

|

Beta

|

t

|

p-value

|

|

EARN

|

-6.213

|

.863

|

-.200

|

-7.201

|

.000

|

|

EARNNEG

|

13.938

|

1.845

|

.387

|

7.555

|

.000

|

|

OWN%

|

48615410781.521

|

6925610606.531

|

.187

|

7.020

|

.000

|

|

BV

|

5.167

|

.627

|

.637

|

8.239

|

.000

|

|

R Squared

|

0.999

|

The analysis supports the previous research finding that the market can reward government ownership in the banking and finance sector, because of possible lessening of the bankruptcy risk, access to the subsidy, thus investors feel more secure about the assets of state controlled banks (beta-value of 0.187).

Transportation

Transportation supports the assumption of the positive impact of government ownership as well, for the Russian transportation sector the impact is significant with the beta-value of 0.359, an interesting fact seems to be that the size of earnings cannot help in market value prediction (a negative beta-value), the only important effect is the absence of loss.

Table 12. Regression Results for Transportation

| |

Standardized Coefficients

|

|

Beta

|

t

|

p-value

|

|

EARN

|

-24.949

|

3.511

|

-1.270

|

-7.105

|

.000

|

|

EARNNEG

|

24.809

|

3.876

|

1.190

|

6.401

|

.000

|

|

BV

|

1.871

|

.176

|

.538

|

10.622

|

.000

|

|

OWN%

|

1630072864.343

|

219391392.912

|

.359

|

7.430

|

.000

|

|

R Squared

|

0.987

|

Transportation sector may display such a large impact of government ownership due to the fact that the sector naturally creates negative externalities, constantly produces insufficient socially desirable quantity of service, and thus has to be subsidized by the government. That results in a very low margin of profit for the transportation sector in Russia.

Retail

The food and retail sector is also affected by the government ownership and this effect is also positive (Table 13), which means that the market rewards state control there, however, the results are not conclusive due to low significance of some elements of the model. The association between state control and market value has a high beta (0.29) at the significance level > .05.

Table 13. Regression Results for Retail

| |

Standardized Coefficients

|

|

Beta

|

t

|

p-value

|

|

EARN

|

-3.997

|

2.007

|

-.191

|

-1.991

|

.094

|

|

OWN%

|

1859359914670.728

|

395513755665.476

|

.290

|

4.701

|

.003

|

|

EARNNEG

|

19.009

|

4.272

|

.745

|

4.450

|

.004

|

|

BV

|

.679

|

.475

|

.193

|

1.429

|

.203

|

|

R Squared

|

0.992

|

We can predict the intercept in food and retail with the probability of 0.99 which is also extremely high, using only the share of government ownership and positive financial result.

The more densely populated sector was the sector of energy, however displayed strong collinearity and proved to be untestable, however, if disregard the model restrictions the government ownership in the energy sector has no significant impact on market value.

Conclusion

Russia is a country with a strong centralized government and the state controlling up to 100 % of the equity in some firms, however the investors do not seem to either penalize or praise such control at least not in the market in total. To see the actual market-relevance of the government ownership we have to include the factor of industry.

The industry effect proved to be significant. In general, the market seems to reward belonging to the service sector and penalize manufacturing. However, there are sectoral differences: government control is severely penalized in mining and metal sector, while in banking, transportation and retail it seems to be rewarded by the market.

We explain these differences by the different effects expected by investors in these sectors. In mining investors, obviously dread the ‘grabbing hand’ effect, in transportation, they hope for state subsidy and in banking – lesser bankruptcy risk. Food and retail praise government ownership probably also due to risk factors.

Our results support the findings of Huang and Xiao (2012) and Truong et al., (2006) which claim that the relationship between government control and market value is higher for transition economies. We find that Russian investors do take into consideration the factor of government control when making investment decisions.

Our results are in line with the efficient market hypothesis, which means that various factors affect the market value of the firms listed in Russian stock exchange, top ten firms by market value display a mean share of government control of 50%.

The future research may include triangulating the findings by qualitative research through interviews with industry officials and large investors to explain the positive or negative impact of state control, as well as a comparison of results on Russian market with other transition economies.

[1] GICS classification

Библиография

1. Alfaraih, M., Alanezi, F., & Almujamed, H. (2012). The Influence of Institutional and Government Ownership on Firm Performance: Evidence from Kuwait. International Business Research, 5(10), 192–200. https://doi.org/10.5539/ibr.v5n10p192

2. Boubakri, N., El Ghoul, S., Guedhami, O., & Megginson, W. L. (2018). The market value of government ownership. Journal of Corporate Finance, 50(405), 44–65. https://doi.org/10.1016/j.jcorpfin.2017.12.026

3. Boycko, Maxim, Shleifer, Andrei and Vishny, Robert, (1996), A Theory of Privatisation, Economic Journal, 106, issue 435, p. 309-19.

4. Carney, Richard W. and Child, Travers Barclay, (2013), Changes to the ownership and control of East Asian corporations between 1996 and 2008: The primacy of politics, Journal of Financial Economics, 107, issue 2, p. 494-513.

5. Eckel, Catherine C. and Vermaelen, Theo, Internal Regulation: The Effects of Government Ownership on the Value of the Firm (October 1, 1986). Journal of Law and Economics, Vol. 29, No. 2, p. 381, 1986. Available at SSRN: https://ssrn.com/abstract=1883677

6. Fama, E. F. (1970) Efficient capital markets: A review of theory and empirical work, Journal of Finance, 25, 2, pp. 383–428.

7. Fama, E. F. (1998) Market efficiency, long-term returns, and behavioral finance, Journal of Financial Economics, 49, pp. 283–306.

8. Guedhami, O., 2012. Characteristics of government acquisitions over time: International evidence and crisis effect. Privatization Barometer Report, 30-42.

9. Hassel, L., Nilsson, H. and Nyquist, S. (2005), “The Value Relevance of Environmental Performance”, European Accounting Review, Vol. 14, No. 1, pp. 41-61.

10. Hess, K., Gunasekarage, A., Hovey, M. (2010). "State-Dominant and Non-State-Dominant Ownership Ownership Concentration and Firm Performance: Evidence from China." International Journal of Managerial Finance, 6(4), 264-89.

11. Huang, L., Xiao, S. (2012). "How Does Government Ownership Affect Firm Performance? A Simple Model of Privatization in Transition Economies." Economics Letters, 116, 480-82.

12. Huang, X., Kabir, R., & Zhang, L. (2016). Government Ownership, Concentration, and the Capital Structure of firms : Empirical Analysis of an

13. Institutional Context from China, (May 2017). Jensen, M., Meckling, W., (1976) Theory of the firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3, 306-360.

14. Jiang, B.B., Laurenceson, J., Tang, K.K. (2008). "Share Reform and the Performance of China's Listed Companies." China Economic Review, 19(3), 489-501.

15. Kendall, M. (1953) The analysis of economic time series – Part 1: Prices, Journal of the Royal Statistical Society, A, 116, pp. 11–25.

16. Liao, J. & Young, M. (2012). The impact of residual government ownership in privatized firms: New evidence from China, Emerging Markets Review 13, 338-351

17. Loh, L., Thomas, T., & Wang, Y. (2017). Sustainability Reporting and Firm Value : Evidence from Singapore-Listed Companies, Sustainability 2017, 9(11), 2112. 1–12.

18. Lourenço, I., Branco, M., Curto, J., & Eugénio, T. (2012). How Does the Market Value Corporate Sustainability Performance? Journal of Business Ethics, 108(4), 417-428.

19. Nash, R., 2017. Contracting issues at the intersection of the public and private sectors: New data and new insights. Journal of Corporate Finance 42, 357-366.

20. Ohlson, J. A. (1995), Earnings, Book Values, and Dividends in Equity Valuation. Contemporary Accounting Research, 11: 661-687

21. Razak, N. H. A., Saidi, N. A., & Mahat, F. (2013). The Relationship Between Government Ownership, Firm Performances and Leverage: an Analysis From Malaysian Listed Firms. Corporate Ownership and Control, 10(4). https://doi.org/10.22495/cocv10i4art4

22. Sappington, D. E., Stiglitz, J. E., (1987) Privatization, information, and incentives. Journal of Policy Analysis and Management 6(4), 567-581. Shleifer, A., Vishny, R. (1994). "Politicans and Firms." Quarterly Journal of Economics, 109, 995-1025.

23. Tahir, S. H., Saleem, M., & Arshad, H. (2015). Institutional Ownership and Corporate Value : Evidence From Karachi Stock Exchange ( KSE ) 30-Index Pakistan. Praktični Menadžment, Stručni Časopis Za Teoriju i Praksu Menadžmenta, 6(1), 41–49.

24. Tran, N. M., Nonneman, W., & Jorissen, A. (2014). Government Ownership and Firm Performance : The Case of Vietnam. International Journal of Economics and Financial Issues, 4(3), 628–650.

25. Truong, D.L., Lanjouw, G., Lensink, R. (2006). "The Impact of Privatization on Firm Performance in a Transition Economy: The Case of Vietnam." Economics of Transition, 14(2), 349-89.

26. V. Brecht, A. Maga, K. Luciani (2018) Exploring the link between ESG disclosure and market value of the firm: evidence from Thai listed companies. ASEAN Journal of Management & Innovation (working paper, in press).

27. Wang, K., & Xiao, X. (2009). Ultimate Government Control Structures and Firm Value: Evidence from Chinese Listed Companies. China Journal of Accounting Research, 2(1), 101–122. https://doi.org/10.1016/S1755-3091(13)60010-6

28. Wei, Z.B., Xie, F.X., Zhang, S.R. (2005). "Ownership Structure and Firm Value in China's Privatized Firms: 1991-2001." Journal of Financial and Quantitative Analysis, 40(1), 87-108.

References

1. Alfaraih, M., Alanezi, F., & Almujamed, H. (2012). The Influence of Institutional and Government Ownership on Firm Performance: Evidence from Kuwait. International Business Research, 5(10), 192–200. https://doi.org/10.5539/ibr.v5n10p192

2. Boubakri, N., El Ghoul, S., Guedhami, O., & Megginson, W. L. (2018). The market value of government ownership. Journal of Corporate Finance, 50(405), 44–65. https://doi.org/10.1016/j.jcorpfin.2017.12.026

3. Boycko, Maxim, Shleifer, Andrei and Vishny, Robert, (1996), A Theory of Privatisation, Economic Journal, 106, issue 435, p. 309-19.

4. Carney, Richard W. and Child, Travers Barclay, (2013), Changes to the ownership and control of East Asian corporations between 1996 and 2008: The primacy of politics, Journal of Financial Economics, 107, issue 2, p. 494-513.

5. Eckel, Catherine C. and Vermaelen, Theo, Internal Regulation: The Effects of Government Ownership on the Value of the Firm (October 1, 1986). Journal of Law and Economics, Vol. 29, No. 2, p. 381, 1986. Available at SSRN: https://ssrn.com/abstract=1883677

6. Fama, E. F. (1970) Efficient capital markets: A review of theory and empirical work, Journal of Finance, 25, 2, pp. 383–428.

7. Fama, E. F. (1998) Market efficiency, long-term returns, and behavioral finance, Journal of Financial Economics, 49, pp. 283–306.

8. Guedhami, O., 2012. Characteristics of government acquisitions over time: International evidence and crisis effect. Privatization Barometer Report, 30-42.

9. Hassel, L., Nilsson, H. and Nyquist, S. (2005), “The Value Relevance of Environmental Performance”, European Accounting Review, Vol. 14, No. 1, pp. 41-61.

10. Hess, K., Gunasekarage, A., Hovey, M. (2010). "State-Dominant and Non-State-Dominant Ownership Ownership Concentration and Firm Performance: Evidence from China." International Journal of Managerial Finance, 6(4), 264-89.

11. Huang, L., Xiao, S. (2012). "How Does Government Ownership Affect Firm Performance? A Simple Model of Privatization in Transition Economies." Economics Letters, 116, 480-82.

12. Huang, X., Kabir, R., & Zhang, L. (2016). Government Ownership, Concentration, and the Capital Structure of firms : Empirical Analysis of an

13. Institutional Context from China, (May 2017). Jensen, M., Meckling, W., (1976) Theory of the firm: managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3, 306-360.

14. Jiang, B.B., Laurenceson, J., Tang, K.K. (2008). "Share Reform and the Performance of China's Listed Companies." China Economic Review, 19(3), 489-501.

15. Kendall, M. (1953) The analysis of economic time series – Part 1: Prices, Journal of the Royal Statistical Society, A, 116, pp. 11–25.

16. Liao, J. & Young, M. (2012). The impact of residual government ownership in privatized firms: New evidence from China, Emerging Markets Review 13, 338-351

17. Loh, L., Thomas, T., & Wang, Y. (2017). Sustainability Reporting and Firm Value : Evidence from Singapore-Listed Companies, Sustainability 2017, 9(11), 2112. 1–12.

18. Lourenço, I., Branco, M., Curto, J., & Eugénio, T. (2012). How Does the Market Value Corporate Sustainability Performance? Journal of Business Ethics, 108(4), 417-428.

19. Nash, R., 2017. Contracting issues at the intersection of the public and private sectors: New data and new insights. Journal of Corporate Finance 42, 357-366.

20. Ohlson, J. A. (1995), Earnings, Book Values, and Dividends in Equity Valuation. Contemporary Accounting Research, 11: 661-687

21. Razak, N. H. A., Saidi, N. A., & Mahat, F. (2013). The Relationship Between Government Ownership, Firm Performances and Leverage: an Analysis From Malaysian Listed Firms. Corporate Ownership and Control, 10(4). https://doi.org/10.22495/cocv10i4art4

22. Sappington, D. E., Stiglitz, J. E., (1987) Privatization, information, and incentives. Journal of Policy Analysis and Management 6(4), 567-581. Shleifer, A., Vishny, R. (1994). "Politicans and Firms." Quarterly Journal of Economics, 109, 995-1025.

23. Tahir, S. H., Saleem, M., & Arshad, H. (2015). Institutional Ownership and Corporate Value : Evidence From Karachi Stock Exchange ( KSE ) 30-Index Pakistan. Praktični Menadžment, Stručni Časopis Za Teoriju i Praksu Menadžmenta, 6(1), 41–49.

24. Tran, N. M., Nonneman, W., & Jorissen, A. (2014). Government Ownership and Firm Performance : The Case of Vietnam. International Journal of Economics and Financial Issues, 4(3), 628–650.

25. Truong, D.L., Lanjouw, G., Lensink, R. (2006). "The Impact of Privatization on Firm Performance in a Transition Economy: The Case of Vietnam." Economics of Transition, 14(2), 349-89.

26. V. Brecht, A. Maga, K. Luciani (2018) Exploring the link between ESG disclosure and market value of the firm: evidence from Thai listed companies. ASEAN Journal of Management & Innovation (working paper, in press).

27. Wang, K., & Xiao, X. (2009). Ultimate Government Control Structures and Firm Value: Evidence from Chinese Listed Companies. China Journal of Accounting Research, 2(1), 101–122. https://doi.org/10.1016/S1755-3091(13)60010-6

28. Wei, Z.B., Xie, F.X., Zhang, S.R. (2005). "Ownership Structure and Firm Value in China's Privatized Firms: 1991-2001." Journal of Financial and Quantitative Analysis, 40(1), 87-108.

|